[ad_1]

RADCOM Ltd. (NASDAQ:RDCM) just lately announced a brand new buyer win with a cellular operator in North America for its RADCOM ACE answer.

This undisclosed Telecom is described as a cellular operator operating an current 4G community, and increasing its 5G protection nationwide.

RADCOM ACE was chosen to assist the cellular operator ship high-quality providers whereas proactively guaranteeing nice buyer experiences.

RADCOM’s background

For these of you unfamiliar with the corporate, here’s a fast compendium of RDCM.

RADCOM providers goal a really particular area of interest of the Telecom market, next-generation cloud assurance for 5G deployments.

The corporate was the primary assurance vendor to go cloud-native.

RDCM is at present promoting its options to “early adopters” in North America, Europe, Asia, and Latin America.

The corporate adopts a multiyear recurring enterprise mannequin, leading to a really predictable income stream, mixed with a really excessive margins product providing (within the 75% vary for its 5G providers).

RADCOM has mainly no debt, and $71 million in money (half of the corporate’s market cap, as we write).

RDCM guided for $45 million to $48 million in revenues in 2022.

We estimate that its two main prospects, AT&T (T) and Rakuten (OTCPK:RKUNY, OTCPK:RKUNF), represented roughly 80% of whole revenues in 2020 and 2021. If our calculations are right, their revenues had been roughly $20 million and $11 million, respectively.

The corporate gained what was most likely the first 5G standalone [SA] assurance contract with Rakuten in Japan, and the primary SA 5G community deployed on the general public cloud [AWS] with DISH (DISH) within the USA.

The marketplace for RADCOM’s providers remains to be in its infancy.

The complexity of 5G networks will drive the necessity for assurance providers, however the transition to SA 5G is simply on the very starting.

Asia and North America are main 5G rollouts, whereas Europe and South America are barely behind in adopting this new know-how.

The next chart is, we consider, a pleasant visualization of the standing of 5G worldwide deployments.

Standalone 5G deployments are only a very small a part of the market (3%), and even contemplating all cellular operators investing in SA 5G networks, in the intervening time, what we are able to visualize is a really small tip of the iceberg:

5G worldwide deployments (Creator chart, supply: International Cell Suppliers Affiliation)

RADCOM’s TAM (whole addressable market) might be very large, over the long run.

Its buyer win are spectacular, associated to the very small variety of cellular operators which have already deployed SA 5G providers.

Even when the corporate will solely be capable of attain a comparatively small piece of its whole addressable market, it may translate right into a multi bagger from right this moment’s degree.

Nevertheless, there are all the time two sides to the coin.

Watching paint dry

RADCOM providers are largely applied by cellular operators in a mature stage of their transition to SA 5G providers.

They will not be perceived as a must have when beginning a SA 5G community, however they develop into important because the complexity of the community and the necessity for AI/ML-driven automation grows.

Along with that, the RDCM promoting cycle could also be fairly lengthy – the deployment of their providers could also be topic to trial durations, typically underneath NDAs, and the rump to revenues might require a number of months/quarters.

Being invested on this firm has, to this point, required a number of endurance.

The dearth of “prompt gratification,” because of the time wanted to go from an preliminary trial to the signing of a multi-year contract that produces a transparent reflection on the corporate’s high line, has made following the corporate as thrilling as watching paint dry.

The market is in a “present me the cash” temper, whereas RDCM developments (reaching key technical milestones, and having fun with a wholesome pipeline of alternatives) don’t instantly translate into revenues.

Now we have tried to visualise what we see as RDCM trajectory to a lastly mature (and rewarding) market within the following chart:

RADCOM milestones (Creator chart, firm’s knowledge )

We consider that the corporate has already constructed a novel product for its area of interest and reached a stable variety of “SA 5G early adopters” world wide, together with its most up-to-date North American win.

This optimistic momentum ought to translate into RDCM delivering stable double-digit income progress in 2023 – we really consider that the corporate will speed up its latest progress trajectory.

Beneath this optimistic situation, we additionally anticipate that extra traders will probably be placing RDCM underneath their radar display, because of the firm lastly proving the effectiveness of its recurring income, excessive margin enterprise mannequin.

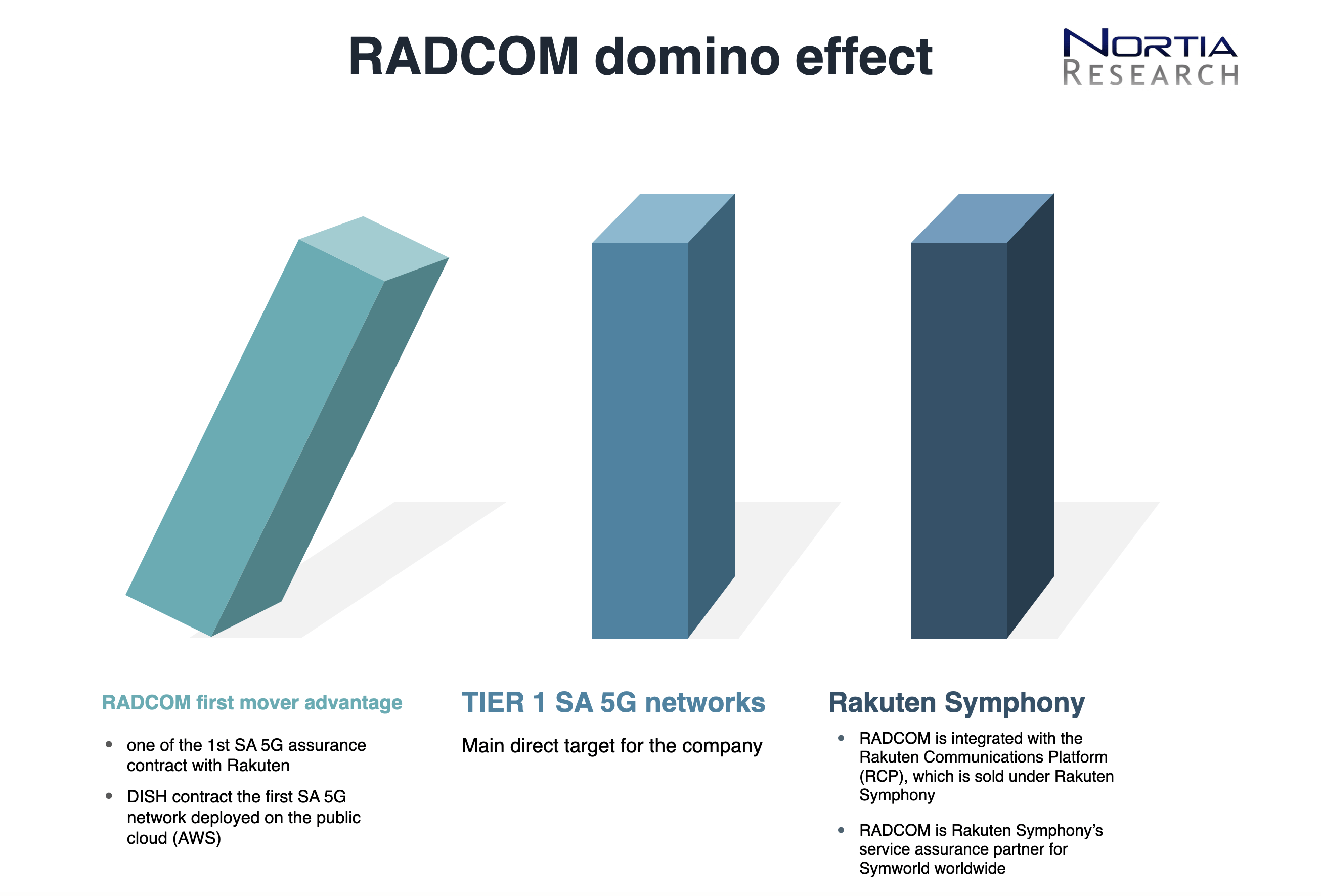

Let’s handle the the reason why we consider the corporate has lastly reached an inflection level, and is now prepared to learn from a powerful domino impact, led by its latest inclusion into Rakuten Symphony product providing.

RADCOM Direct and Oblique sale channels

RDCM ought to take pleasure in a primary mover benefit relating to its particular product providing, having partnered with among the very early adopters of SA 5G networks.

RADCOM’s two primary contracts had been signed with an incumbent Telecom like AT&T and an revolutionary participant like Rakuten.

We consider these buyer wins ought to present the market with a transparent indication that RDCM product providing could also be match each for a conventional cellular operator shifting to SA 5G, in addition to for a brand new participant embracing a brand new, revolutionary strategy to constructing a SA 5G community.

RADCOM is directing its gross sales efforts primarily to Tier 1 Telecoms, as explained by on this 2019 interview [edited for clarity]:

Certainly one of RADCOM’s most conspicuous options is that, regardless that it’s not an enormous firm, it has Tier-1 prospects, amongst them AT&T, Globe Telecom (OTCPK:GTMEF, OTCPK:GTMEY), and Japanese firm Rakuten.

One of many duties [former CEO Yaron Ravkaie] has assumed: to take an organization that had already invented a big proportion of the know-how and provides it the “DNA of mega-scale orientation” as a way to serve the massive prospects.

Profitable firms on this sector give attention to Tier-1 [customers].

Nevertheless, RADCOM’s affiliation with Rakuten has been, in our opinion, a sport changer for RDCM, opening the way in which to a really rewarding oblique sale channel, which will have delivered among the most up-to-date wins, together with the unannounced North American operator.

It’s as if RADCOM had doubled the variety of domino raws which will generate its anticipated chain response.

It doesn’t actually matter which uncooked begins falling first: the top sport is an elevated (and simpler) market penetration.

MARHARYTA MARKO/iStock by way of Getty Pictures RADCOM domino impact (Creator chart )

Rakuten strategy to constructing a 5G community.

Rakuten constructed the world’s first Open Radio Entry Community [ORAN] community.

Tareq Amin, CEO of Rakuten Cell, pushed a very revolutionary idea into existence.

Right here is how he explains his imaginative and prescient [edited for clarity]:

One of many first key components I needed to vary is adopting this distinctive cloud structure, as a result of no one had actually deployed an end-to-end horizontal cloud throughout any telco but.

The second component is that this factor known as Open RAN, which is the thought of disaggregating {hardware} and software program.

The third component, my final dream, is the enablement of a full autonomous community that is ready to run itself, repair itself, and heal itself with out human beings.

The concept that many extra distributors can compete to construct the radio entry {hardware} that Rakuten Cell can use to run its personal software program on results in a community that’s less expensive each to construct and to run:

I do know my price right this moment is 40 % cheaper in operating my community than any competitor in Japan.

Dish’s community is the third ORAN community in-built your complete world.

As we underlined in the beginning of our article, Dish represented RADCOM’s first SA 5G community deployed on the general public cloud, by way of Amazon (AMZN) AWS providers.

Because the Verge article we already quoted underlines, “Rakuten Symphony helps Dish run its community right here together with one other community known as 1&1 in Germany.”

It’s our educated guess that the unannounced European buyer for RDCM’s assurance providers might be Germany’s 1&1.

1&1 at present operates as a digital cellular community operator and broadband supplier.

Nevertheless, the corporate is working in direction of changing into Germany’s fourth nationwide cellular operator.

1&1 just lately managed to satisfy its deadline of launching preliminary fastened wi-fi entry [FWA] providers earlier than the top of 2022 in just a few German cities like Frankfurt am Predominant and Karlsruhe.

Though it missed its goal to put in not less than 1,000 base stations throughout Germany by the top of 2022, it’s required to achieve not less than 25% of households by the top of 2025 and canopy 50% of the nation’s inhabitants with 5G providers by 2030.

Appledore Analysis has an attention-grabbing replace on 1&1 rollout:

In dialog with Symphony CEO Tareq Amin, Chief Income Officer Rabih Dabbousi, 1&1 CEO Michael Martin gave new particulars of 1&1’s progress and pondering on key points of its plans.

The totally cloud-native core community is in place and dealing. 1&1 is already the most important telco edge cloud community in Europe. The most important problem now’s the rollout of antenna websites.

1&1 has been holding a pleasant consumer trial over the past two months.

For his or her pleasant consumer trials, they’ve began with gaming, for instance their community’s capacity to assist low latency.

The outcomes are actually spectacular, with usually a 3msec latency sustained between gamer and utility server over the community.

In additional prosaic phrases – a Minecraft participant utilizing the 1&1 community has the sting over one other participant on a higher-latency connection!

As oblique affirmation of our hypothesis about 1&1 being the unannounced European RADCOM buyer, we discovered a few references on LinkedIn from current and former RDCM workers resulting in the this conclusion.

We anticipate that RCDM will probably be beginning producing a significant income stream from 1&1 throughout 2023.

If two coincidences are a clue, three coincidences could also be a proof

Whereas we’d love to find that the unannounced North American buyer is both Verizon (VZ) or T Cell (TMUS), given the dimensions of those two U.S. networks, we’d be extra inclined to have a look at a Canadian cellular operator because the potential new shopper.

Canadian community operator Telus (TU, T:CA) has just lately been exploring options with Rakuten Symphony [edited for clarity]:

Telus is the most recent telco to discover the potential of deploying Open RAN know-how in its community and is within the technique of creating a broad trial with Rakuten Symphony in response to Tareq Amin.

“Now we have been engaged with Telus for nearly three months,” Amin informed TelecomTV throughout a dialog held on the Digital Transformation World occasion in Copenhagen [in September 2022].

“Telus is an excellent instance” of the sort of firm a telco must be today, he added. “The corporate’s administration may be very open minded”.

A partnership between Rakuten and Telus would even be very attention-grabbing to observe because the Canadian operator shouldn’t be a “greenfield” operator, constructing its 5G community from scratches:

“We want a brownfield [example]. You understand, it might be Telus. It might be Telefonica. It might be a type of operators that wish to do one thing completely different. And if we’ve sufficient of such instances, wherein TCO [total cost of ownership] is validated, then I feel individuals will cease speaking about how Open RAN isn’t match for function in business cellular networks”.

Telus would require distributors to assist Open RAN specs, as confirmed by the corporate’s VP of community and structure technique, Bernard Bureau.

As a nationwide wi-fi service, TELUS competes with BCE Inc. (BCE) and Rogers Communications Inc. (RCI), and reaches round 9.2 million wi-fi subscribers.

Conclusion

Indicating the RADCOM Ltd. unannounced buyer as Telus on the one foundation that the Canadian community operator has began a trial of Rakuten’s know-how might sound like a hypothesis based mostly on a weak clue – nonetheless, there should not many different candidates that match RADCOM’s description (North American operator with an current 4G community and creating a 5G nationwide rollout).

We consider there may be a number of sense for RDCM traders to intently observe any new growth on the Rakuten Symphony entrance: the Dish and 1&1 buyer wins are there to show that RADCOM might solely profit from being bought underneath Rakuten’s built-in product providing.

When you embrace Rakuten Symphony providing, it makes little sense for any buyer to deviate from their package deal for service assurance, and community insights merchandise.

Even when our hypothesis on Telus was incorrect, we’d welcome any Tier 1 partnership with one other U.S. or Canadian nationwide wi-fi service as affirmation of our thesis: RADCOM Ltd. domino impact could also be lastly in place, as extra networks transfer to SA 5G and watch early adopters as an inspiration for his or her alternative relating to a completely automated assurance platform.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please concentrate on the dangers related to these shares.

[ad_2]

Source link