[ad_1]

Share this text

Whereas all investing carries some threat, that doesn’t imply all threat is created equal. Learn to optimize your portfolio weighting for the most effective risk-adjusted returns utilizing fashionable portfolio principle and the Sharpe ratio.

Fashionable Portfolio Idea

To calculate essentially the most environment friendly crypto portfolio, we’ll make the most of facets of Fashionable Portfolio Idea (MPT). The idea assumes that an investor is risk-averse and is seeking to discover the optimum ratio between theoretical features and assumed threat. MPT does this by taking a batch of property and calculating the most effective weighting for every utilizing historic knowledge. From this level, we will regulate weightings to extend or lower theoretical returns towards the volatility of every asset.

Riskier investments usually have the potential for higher returns. Thus, fashionable portfolio principle seeks to create a weighted portfolio that finds the best theoretical returns for the least quantity of threat.

For instance, a portfolio weighting might yield a 90% return based mostly on historic knowledge however have an implied threat (as measured by volatility) of 0.8. One other weighting might result in solely 70% returns however have a a lot decrease threat, making it a greater risk-adjusted funding. This ratio between anticipated return and threat is extra generally referred to as the Sharpe ratio.

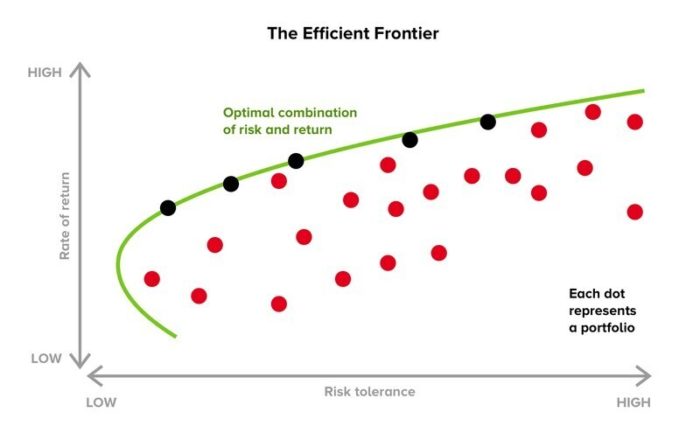

The upper an asset, or group of property, the upper its theoretical returns are per unit of threat. By experimenting with totally different asset weightings, we will discover optimum portfolio compositions relying on how a lot threat an investor is keen to take. We will use a Monte-Carlo strategy to generate an “environment friendly frontier” of portfolio compositions that maximizes risk-adjusted returns.

Every dot on the graph represents a hypothetical portfolio. Dots in black on the highest fringe of the plot are a part of the environment friendly frontier. These portfolios have the most effective risk-adjusted returns, which means that an investor shouldn’t be taking up extra threat with out the chance of optimum returns.

The Sharpe Ratio and Crypto Portfolios

Whereas fashionable portfolio principle and the Sharpe ratio have been initially designed to be used in conventional monetary markets, buyers can even use them to optimize a crypto portfolio.

Nonetheless, calculating an correct Sharpe ratio depends closely on historic worth knowledge. To generate a very good Sharpe ratio for portfolio allocation of a given crypto asset, we want knowledge on its efficiency throughout a full bull/bear cycle to evaluate its volatility and the following threat of holding it.

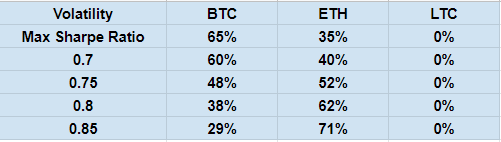

Sadly, the crypto house is each nascent and fast-moving, which means that few property with sufficient historic knowledge are eligible for consideration. This evaluation will use a portfolio of Bitcoin, Ethereum, and Litecoin to reveal the most effective risk-adjusted returns as these property have the best market capitalization with essentially the most historic knowledge. Utilizing these three property, the approximate finest allocation for maximizing risk-adjusted returns comes out at 65% Bitcoin, 35% Ethereum, and 0% Litecoin.

Nonetheless, shifting alongside the environment friendly frontier will show environment friendly portfolios with larger risk-adjusted returns. Typically, riskier portfolios on the frontier will substitute Bitcoin for Ethereum. Historic knowledge signifies that Ethereum can generate larger returns than Bitcoin however can be extra vulnerable to massive drawdowns, growing its volatility and, due to this fact, the chance of holding it.

Now we’ve examined how fashionable portfolio principle and the Sharpe Ratio might help us obtain the most effective risk-adjusted returns, let’s take a look at examples of low, medium, and high-risk portfolios.

Low-Danger

The bottom threat crypto portfolio with the best returns follows the environment friendly frontier as described beforehand. Utilizing present historic knowledge, low-risk buyers ought to allocate round 65% to Bitcoin and 35% to Ethereum to create the most secure portfolio with essentially the most upside potential. Buyers wanting to extend their risk-adjusted returns can strive allocating much less to Bitcoin and extra to Ethereum. At this level, all different crypto property are both too dangerous or have related threat profiles however worse historic returns than Bitcoin and Ethereum, resembling Litecoin.

Medium-Danger

A medium-risk portfolio will nonetheless use the environment friendly frontier to maximise risk-adjusted returns however strikes away from a excessive Bitcoin allocation. 10% Bitcoin, 89% Ethereum, and presumably 1% Litecoin could be one technique to obtain a medium-risk portfolio. The excessive proportion of Ethereum will improve theoretical returns but additionally implied volatility. Moreover, a small allocation of Litecoin might assist yield the next return within the situation the place it experiences vital upward worth divergence.

Excessive-Danger

That is the place issues get fascinating. As talked about beforehand, when calculating lower-risk portfolios, we solely wish to use property which have worth knowledge going again a number of years. Nonetheless, there may be nonetheless some advantage to wanting on the Sharpe ratios for newer crypto property, so long as we perceive that doing so exposes an investor to much more threat.

For a higher-risk portfolio, an investor can substitute an growing quantity of Ethereum for different crypto property. To assist establish candidates for a high-risk allocation, we will take a look at the one-year Sharpe ratios of different crypto property and see how they evaluate to Bitcoin and Ethereum.

When selecting riskier property for a portfolio, something with a Sharpe ratio larger than Bitcoin and Ethereum is a possible candidate. Inside the prime 10 crypto property by market capitalization, Solana and Terra have ratios of three.37 and three.25, respectively, with Cardano coming in third at 2.85.

As a result of Solana, Terra, and Cardano have one-year Sharpe ratios larger than Ethereum, they may very well be good riskier property to choose based mostly purely on the historic knowledge. Nonetheless, you will need to be aware that different elements are vital when deciding whether or not to put money into an asset. Issues such because the undertaking fundamentals, time since launch, and whether or not or not the asset worth appears to be like overextended ought to all be thought-about when selecting an funding.

Like earlier than, a portfolio will turn into riskier however probably yield larger returns the extra Ethereum is substituted for these newer, riskier property.

Whether or not you’re on the lookout for the most effective low-risk allocation or keen to dive into some riskier bets, you’ll want to seek out someplace to construct your portfolio. That is the place Phemex is available in. You should buy all the property talked about on this function plus many extra. Furthermore, the platform’s low charges and wonderful help providers make for an important selection. For these not prepared to leap in simply but, Phemex provides simulated crypto buying and selling the place customers can study and take a look at totally different buying and selling methods, risk-free.

For extra superior customers, Phemex provides perpetual contract trading on all crypto property and inverse perpetuals on Bitcoin. By depositing and buying and selling on Phemex, customers can earn as much as $100 and obtain extra price reductions and bonuses by referring associates. For extra info, try the official Phemex website.

Disclaimer: On the time of scripting this function, the writer owned BTC, ETH, and several other different cryptocurrencies. The data contained on this article is for instructional functions solely and shouldn’t be thought-about funding recommendation.

Share this text

[ad_2]

Source link